![]()

- Dutch Bros Inc. (NYSE: BROS) tanks after hours on rising costs that prompt 2022 Ebitda forecast cut

- Stock trading as low as $22, below $23 price paid by IPO investors last year

- Revenue growth remains totally intact, with a big Q1 beat and full-year outlook unchanged

- Brand recognition continues to get stronger as expansion from home in Oregon continues

- Stock now looks reasonable at enterprise value of 4x 2023 consensus revenue

- Analysts expect sales growth of roughly 30% annually for next several years

- Tremendous opportunity of 4,000 shops vs. just 572 locations across 12 states

By John Jannarone of IPO Edge

Since its wildly successful IPO and ensuing run, Dutch Bros Inc. (NYSE: BROS) has been too hot for many investors to handle. But after Wednesday’s rout, there’s a rare opportunity to own a unique growth business with a future of sweet returns.

Shares of the popular drive-thru beverage company plunged as much as 36% to $22 a share in after-hours trade Wednesday after the company slashed profit guidance due to rising commodity costs. The main cause of the rout: 2022 Ebitda expectations being lowered to “at least” $90 million versus a prior target of $115 million to $120 million.

The culprits were major ingredients such as dairy, which accounts for 28% of costs and has surged to record prices. The company also made a decision not to raise prices as much as most competitors and saw some inefficiencies at newly-opened stores, which were especially large in number during the quarter. While the company sees the costs as temporary, it nonetheless made a serious guidance cut.

Before ditching Dutch Bros, savvy investors should smell a rare opportunity. First, the growth story is far from over and hasn’t even been interrupted. The company actually beat revenue estimates of $145 million (actual $152.2 million) and barely missed same-shop-sales growth estimates of 6.5% (actual was 6%). That suggests new stores, which don’t appear in same-shop-sales for the first year, are going gangbusters.

This year’s sales are still expected to grow a whopping 40%, with increases of roughly 30% for the next several years, according to consensus estimates. That’s due to expectations for robust same-shop sales growth as well as steady additions to its store count, which has vast room to rise.

Indeed, the company had just 572 locations across 12 states at the end of the first quarter. Over the next 10-15 years, there’s potential to reach 4,000 shops, an incredible 7x opportunity.

Importantly, the company is very prudent in its selection of locations, mainly adding shops in contiguous states that branch gradually away from its home of Grants Pass, Oregon. And as the first quarter results confirm, it has no trouble drawing customers to those new venues in droves.

Dutch Bros., also skews to a younger demographic, selling a range of beverages from cappuccinos to energy drinks (but not drip coffee favored by Boomers). The model itself – a high-speed drive-thru-only setup – also resonates with people on the go or sneaking out for a quick treat.

“High-capacity drive-thru units are what consumers want and that is exactly what Dutch Bros is developing,” Gordon Haskett analyst Jeff Farmer wrote in a recent note.

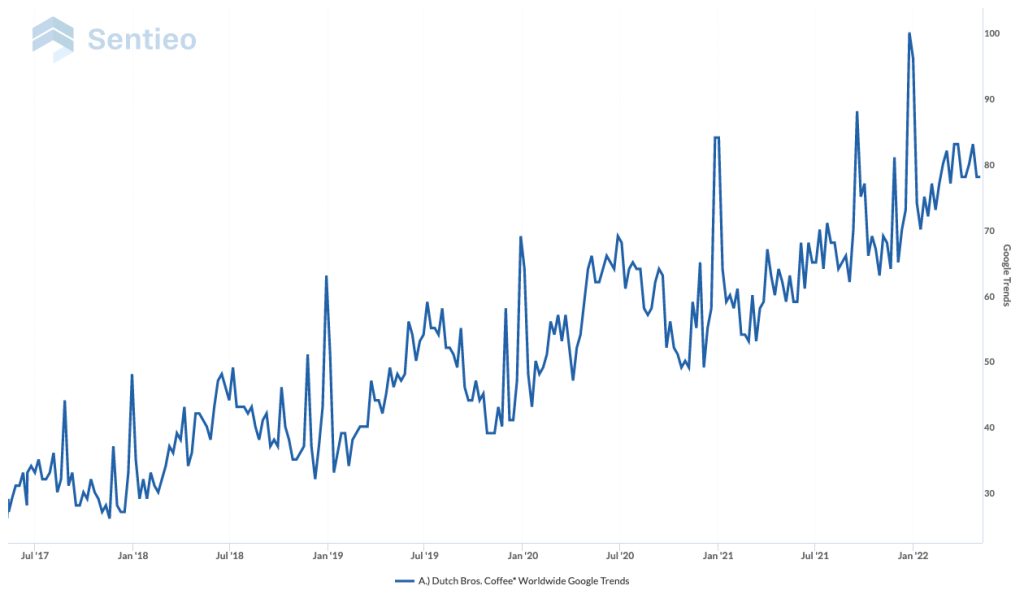

The brand, once niche, has also become very strong. As seen the chart below from Sentieo, an AI-enabled research platform, Google Trends for Dutch Bros have surged consistently for the last few years.

Of course, growth stories have fallen out of favor during the recent market meltdown. But investors should take comfort in the company’s healthy profit profile. While the cut to near-term Ebitda may be painful, it’s expected to quadruple to $400 million in 2026, according to consensus forecasts.

Indeed, the shops themselves are veritable cash machines. Expectations for store-level Ebitda in the long run should remain in the 28% to 32% range.

After Wednesday’s rout, Dutch Bros trades at an enterprise value of just below 4 times 2022 consensus Ebitda, according to Sentieo. That’s reasonable for a profitable business with such vast room to expand.

In a market fraught by inflationary challenges, investors are bound to be burned occasionally. But with a growing brand awareness, core profitability and tremendous growth potential, Dutch Bros shares may soon turn into a real treat.

Contact:

IPO Edge

Twitter:@ipoedge

Instagram: @ipoedge