Is Home Depot (HD) a Buy at $300?

By IPO Edge Editorial Staff

Home improvement’s biggest name has lost a quarter of its value in twelve months.

Home Depot (HD) dropped from a 52-week high near $427 to roughly $300 ahead of this morning’s Q1 fiscal 2026 earnings report.

The release brought a modest beat. Sales grew 4.8% to $41.8 billion and comparable sales eked out a 0.6% gain.

Profits told a different story. GAAP earnings per share dropped to $3.30 from $3.45, marking another quarter of margin pressure.

Management reaffirmed full-year guidance that still calls for adjusted EPS to decline about 5%.

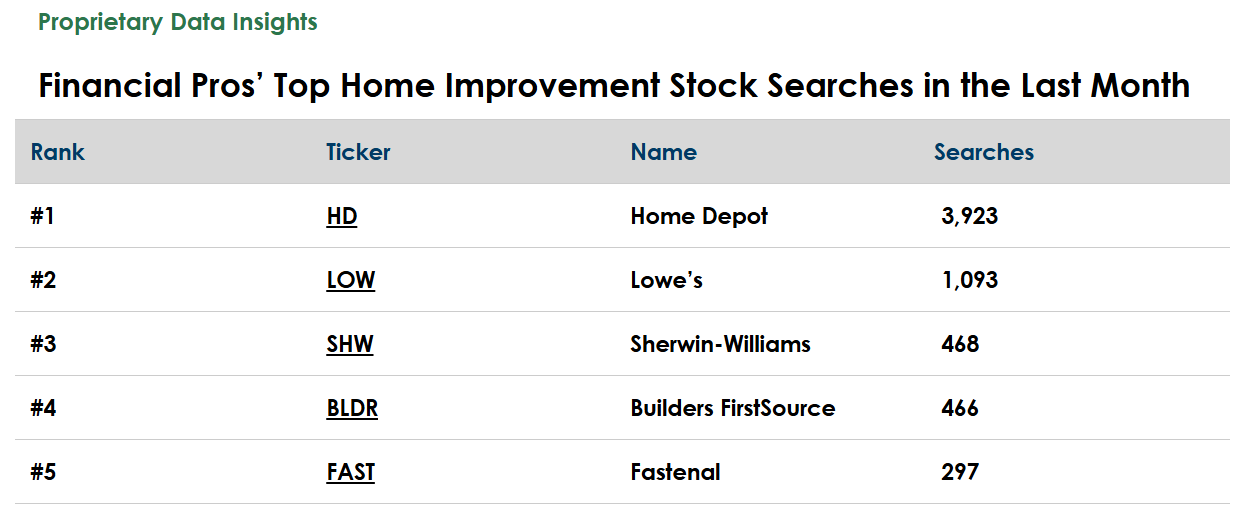

Search volume from financial pros surged ahead of the print, per our TrackStar data, with HD drawing nearly four times the interest of rival Lowe’s.

After a brutal 2026, here’s why we think the setup looks more interesting than it has in years.

Home Depot’s Business

Founded in 1978, Home Depot operates 2,356 warehouse-format stores across the United States, Canada, and Mexico.

The company serves do-it-yourself homeowners and professional contractors with everything from lumber and appliances to plumbing fixtures and power tools.

Roughly half of revenues come from Pro customers, with the other half from DIY shoppers. Recent acquisitions of SRS Distribution and GMS have dramatically expanded the company’s reach into roofing, pool, landscape, and specialty building products.

Home Depot segments its business into the following areas:

- Building Materials (32% of total revenues) – Lumber, drywall, paint, hardware, and core construction supplies

- Décor (31% of total revenues) – Kitchen, bath, flooring, appliances, and interior finishing products

- Hardlines (29% of total revenues) – Tools, outdoor power equipment, lawn and garden, and seasonal goods

- Other (8% of total revenues) – SRS Distribution, GMS, and HD Supply specialty distribution operations

The third quarter of fiscal 2025 fell short of internal expectations. CEO Ted Decker blamed a quiet storm season, soft housing turnover, and cautious consumers wary of big-ticket projects.

That forced management to cut full-year profit guidance in November, sending shares down 6% in a single session.

The real growth story sits in the Pro channel. Home Depot closed the $18 billion SRS Distribution deal in mid-2024, then layered on $5.5 billion for GMS in September 2025.

GMS alone contributed $892 million in sales during its first eight weeks under Home Depot ownership.

The strategy aims to capture the larger, more recurring spend of professional contractors as DIY demand normalizes from pandemic-era highs.

On tariffs, management says it has diversified sourcing and worked with vendors to absorb cost increases without major price hikes.

Financials

Source: Stock Analysis

Trailing twelve-month revenue reached $166.6 billion, up 2.2% from fiscal 2024.

Growth has slowed from the 14% to 20% gains posted in 2020 and 2021, but Home Depot has avoided the outright revenue declines plaguing many discretionary retailers.

Gross margin held steady at 33.1%, almost identical to the 33.4% reported in fiscal 2024.

Operating margin compressed from 13.5% to 12.5% as the company absorbed integration costs and higher SG&A from SRS and GMS.

Free cash flow rebounded to $14.3 billion on a trailing basis, up 13.2% year-over-year and well above the $11.5 billion generated in fiscal 2022.

That cash easily covers $2.6 billion in capital expenditures and $6.9 billion in dividends paid through the first nine months of fiscal 2025.

Share repurchases have been suspended this year to preserve cash for the GMS deal, a meaningful change from the $649 million spent in the prior period.

The balance sheet carries $56 billion in total debt against $1.7 billion in cash, with interest expense running at $1.8 billion for the first nine months.

Leverage is elevated but manageable given the cash flow profile.

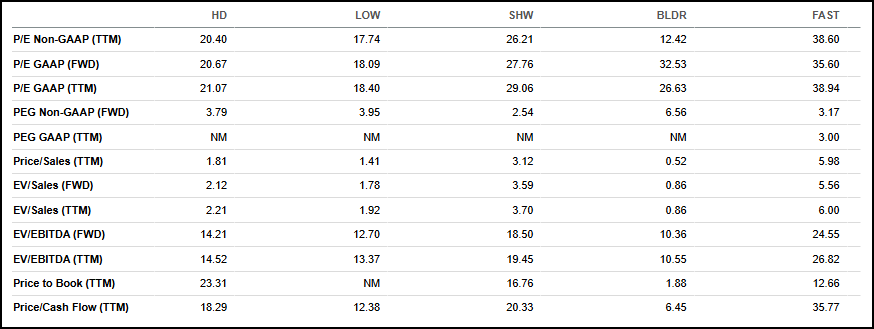

Valuation

Source: Seeking Alpha

After the stock’s 21% drop over the last year, Home Depot trades at 20.4x trailing non-GAAP earnings and 18.3x cash flow.

That sits at a notable discount to Sherwin-Williams (SHW) at 26.2x earnings and Fastenal (FAST) at 38.6x, two specialty peers with stronger margin profiles.

Lowe’s (LOW) is cheaper at 17.7x earnings, but its smaller footprint and weaker Pro business have historically warranted that gap.

Builders FirstSource (BLDR) looks optically cheap at 12.4x earnings, though its cyclical exposure to new home construction makes the multiple appropriate.

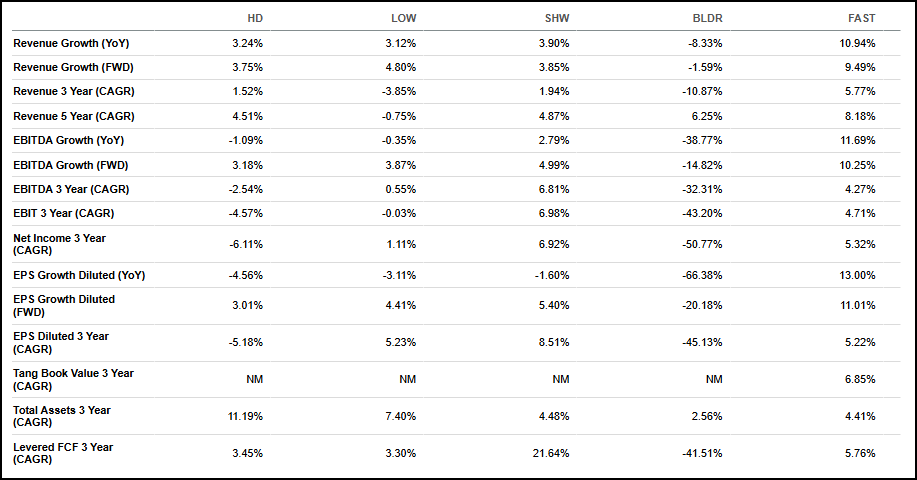

Growth

Source: Seeking Alpha

Home Depot’s 3.2% trailing revenue growth and 3.8% forward expectation land in the middle of the peer group.

That trails Fastenal’s 10.9% growth and Sherwin-Williams’ 3.9% pace, but easily beats Builders FirstSource’s 8.3% decline.

The five-year revenue CAGR of 4.5% beats Lowe’s at negative 0.8% and trails only Builders FirstSource and Fastenal.

Forward free cash flow growth of 3.5% suggests modest expansion ahead, with the Pro acquisitions providing a tailwind once integration costs normalize.

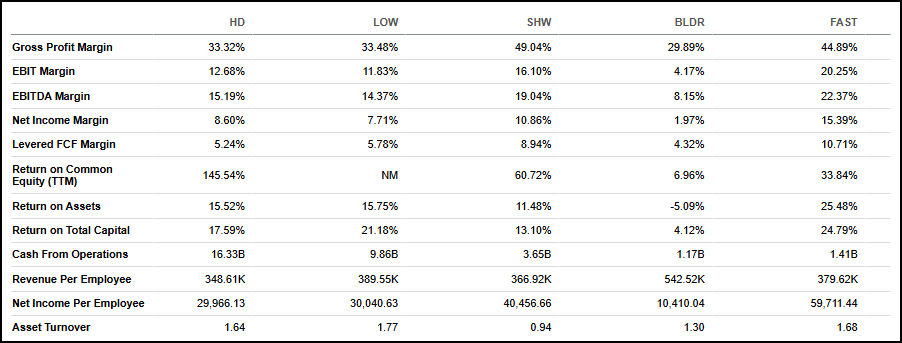

Profitability

Source: Seeking Alpha

Home Depot’s 33.3% gross margin trails Sherwin-Williams at 49.0% and Fastenal at 44.9%, reflecting its lower-margin retail mix.

Where Home Depot dominates is scale and capital efficiency. Cash from operations hit $16.3 billion, more than 4x the $3.7 billion Sherwin-Williams produced and 14x what Builders FirstSource generated.

Return on common equity reached 145.5%, the highest of the group by a wide margin, helped by the company’s aggressive historical buybacks.

EBIT margin of 12.7% sits behind Sherwin-Williams and Fastenal but ahead of Lowe’s and Builders FirstSource.

Continued…

Our Opinion 8/10

Home Depot has compressed from a stretched valuation to one that looks fair for a business of this quality.

The Pro pivot through SRS and GMS gives the company a credible second growth engine that’s less tied to housing turnover.

A 3.1% dividend yield, fortress cash generation, and a balance sheet that can support both debt service and capital returns make this a stock worth owning through the cycle.

The near-term setup isn’t pretty. Earnings will likely decline again this year, buybacks are paused, and housing affordability isn’t improving anytime soon.

But at $300, you’re paying a reasonable price for a business that compounded shareholder returns at exceptional rates for decades.

We’d be buyers on weakness.

READ MORE

Final Panel Agenda and Closing Registration: 2nd Princeton CorpGov Forum May 21 – Endowments, Activism and Entertainment

Never Miss our Weekly Highlights HERE

Contact:

Editor@IPO-Edge.com

Click HERE to follow us on LinkedIn