Is Campbell’s (CPB) the Cheapest Comfort Food on the Shelf?

By IPO Edge Editorial Staff

Comfort food is having a moment. Campbell’s (CPB) stock isn’t.

Americans keep cooking at home, a habit that should favor the soup and sauce aisle. Yet shares sit near the bottom of the packaged food group.

Never Miss our Weekly Highlights HERE

This morning’s third-quarter report gave the bears plenty to work with. Organic sales fell 4%, adjusted EBIT dropped 24%, and adjusted EPS hit $0.50, down 32% from a year ago.

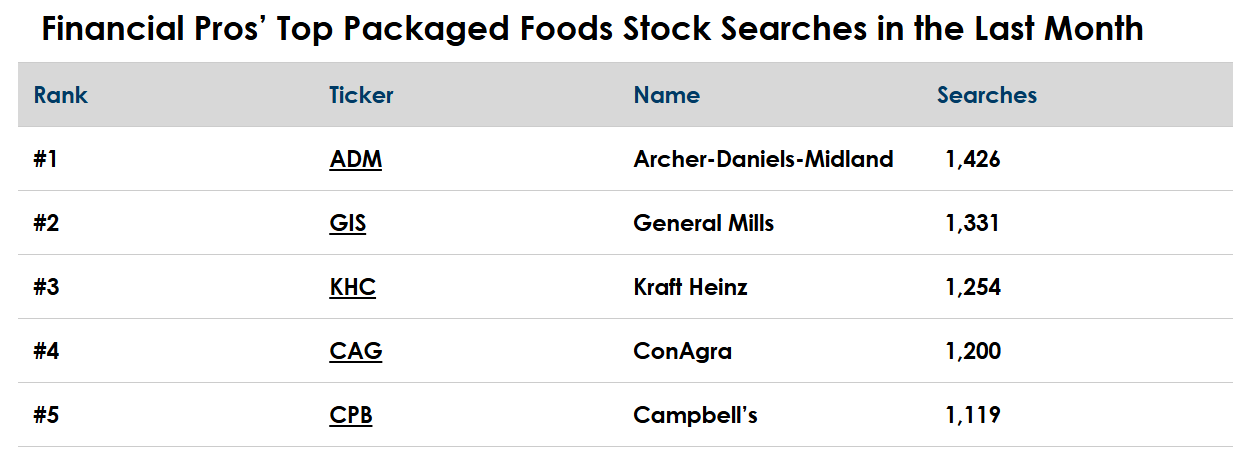

That put Campbell’s at #5 in our packaged foods searches, behind Archer-Daniels-Midland (ADM), General Mills (GIS), Kraft Heinz (KHC), and ConAgra (CAG), per our TrackStar data.

Here’s the twist. Campbell’s is the only name on this list still growing. The question is whether the market is right to look away.

Campbell’s Business

The Campbell’s Company traces its roots to 1869 and the condensed soup can that became an American pantry staple. It sells far more than soup now, with premium names driving the growth.

It reaches grocery, mass, club, and e-commerce retailers across North America, with brands that include Campbell’s, Swanson, Pacific, Rao’s, Prego, Goldfish, and Pepperidge Farm.

READ MORE

Highlights: Tech Edge at Pax8 Beyond 2026 in Salt Lake City

Campbell’s segments its business into the following areas:

- Meals & Beverages (62% of total revenues) – Soups, broths, sauces, and beverages led by Campbell’s, Swanson, Pacific, Prego, and Rao’s

- Snacks (38% of total revenues) – Cookies, crackers, and salty snacks led by Goldfish, Pepperidge Farm, Snyder’s, and Lance

The quarter stayed soft. Soup consumption slipped 4.4% against a strong year-ago period, and salty snack sales fell 6.2%.

Management is leaning into at-home cooking with more brand support and a summer launch of Campbell’s Condensed Sauces.

READ MORE

Space Farming Takes Off: Redwire Wins Landmark Mission

New Snacks leadership is cutting complexity and refocusing Goldfish on families with kids, where consumption has held flat for two quarters.

Cost cuts are the other lever, with roughly $200 million booked against a $375 million multi-year savings target, plus another $100 million in overhead reductions.

Financials

Source: Stock Analysis

Revenue tells the cleanest story. Trailing twelve-month sales of $9.9 billion top the $8.1 billion of fiscal 2019, even with sales off 2.9% on the year.

Margins are the soft spot. The 28.9% gross margin has slipped from above 30%, and that pressure flows straight down to a 6.1% net margin.

Cash generation still works.

The company produced $671 million in free cash flow over the trailing year, enough to cover its $1.54 per share dividend with room to spare.

READ MORE

Applied Digital Secures Up to $550M as AI Infrastructure Race Accelerates

The catch is the balance sheet. About $7.0 billion in debt against $402 million in cash puts net leverage near 4.0x EBITDA.

To protect its investment-grade rating, management froze the dividend and scrapped buybacks.

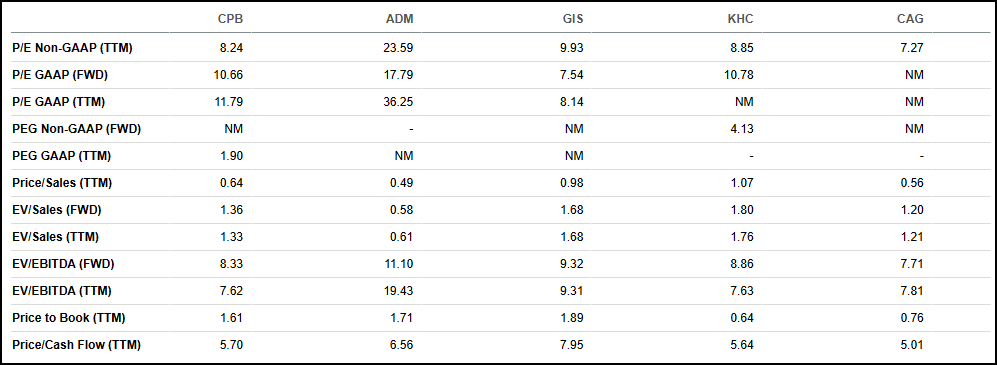

Valuation

Source: Seeking Alpha

On earnings, Campbell’s looks cheap. It trades at 8.2x trailing earnings, under General Mills at 9.9x and ADM at 23.6x, though ConAgra edges it out at 7.3x.

The cash flow read is similar.

At 5.7x price-to-cash flow, Campbell’s sits just above Kraft Heinz at 5.6x and ConAgra at 5.0x, and below General Mills at 8.0x.

Cheap is the theme across this group, and Campbell’s lands squarely in the discount bin.

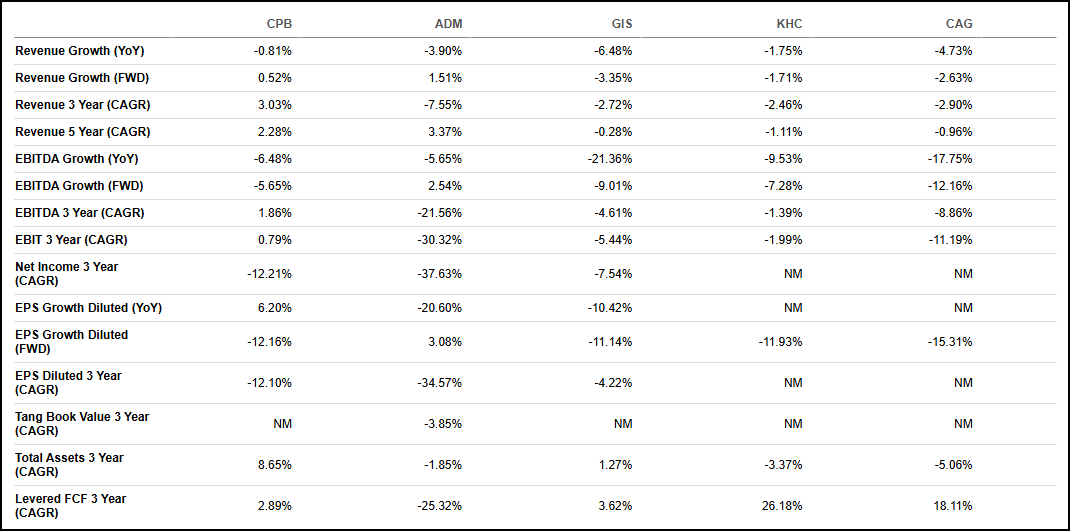

Growth

Source: Seeking Alpha

This is where Campbell’s separates from the pack. Its three-year revenue CAGR of 3.0% is the group’s only positive mark, while ADM shrank 7.6% and General Mills fell 2.7%.

READ MORE

Solidion Strengthens Battery Moat with 7 New Patents

The forward view holds up too, with analysts modeling 0.5% growth ahead, second only to ADM. Campbell’s also posted the only positive year-over-year EPS growth here, up 6.2%.

Free cash flow growth is less flattering. Its three-year levered FCF CAGR of 2.9% trails Kraft Heinz at 26.2% and ConAgra at 18.1%, though both lap weaker bases.

Continued…

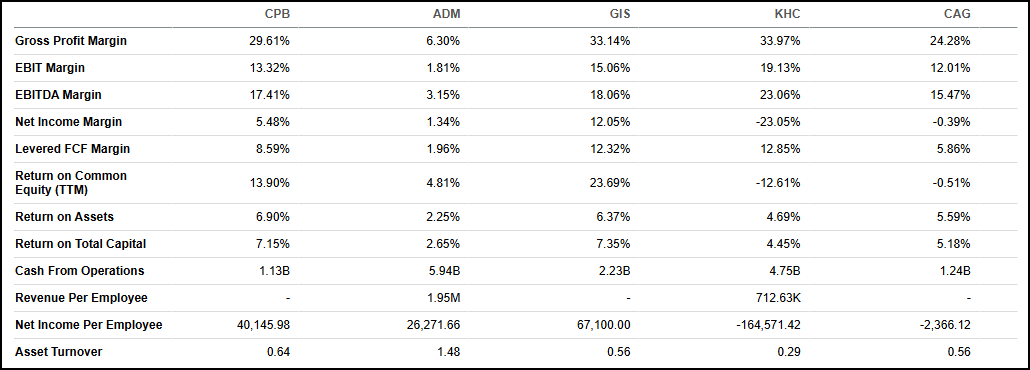

Profitability

Source: Seeking Alpha

Campbell’s profitability lands mid-pack. The 29.6% gross margin trails General Mills at 33.1% and Kraft Heinz at 34.0%, yet towers over ADM at 6.3%.

Further down, its 5.5% net margin beats the losses at Kraft Heinz and ConAgra but falls short of General Mills at 12.1%.

READ MORE

Winning Government Business: HighGround Market Founder & CEO John Price, Live at NYSE

Free cash flow margin tells the same story. At 8.6%, Campbell’s converts more sales to cash than ADM and ConAgra, but less than General Mills and Kraft Heinz.

Our Opinion 6/10

Campbell’s is the cheap, modest grower in a sector full of shrinking giants.

We like that it outgrows its peers on the top line and still throws off real cash. The at-home cooking trend and premium brands like Rao’s give it a genuine edge.

But the margin damage is hard to ignore. Adjusted EBIT will drop 17% to 20% this year as tariffs and inflation squeeze the gross line.

The 4.0x leverage is the bigger worry. With the dividend frozen and buybacks gone, capital return stalls until debt comes down.

We’d want margins to stabilize before paying up here.

Contact:

Editor@IPO-Edge.com

Click HERE to follow us on LinkedIn