If we think of a company that sells food containers, shoe racks, bathmats, or cases for the organization of cables, we would not think of a company with continuous innovation and advanced technology capabilities. However, these are two of the pillars of Betterware de Mexico.

History of The Company

Betterware was founded in 1928 in East London as a multilevel marketing company selling household products, and it wasn’t until 1995 that it arrived in Mexico. With this, there were changes made, because with the British company, there was a cost to join the sales team as well as to purchase new catalogs, which are practices that disappeared in Mexico.

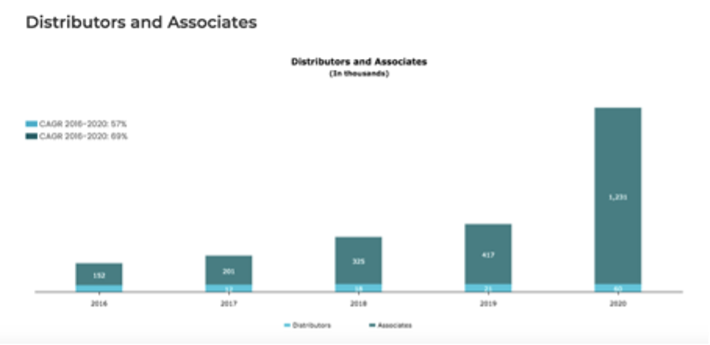

In 2001, Luis Campos, current Chairman of Betterware, bought the Latin American division, establishing the distribution center in Guadalajara, Jalisco (2003). Since then, the company has had significant growth, with a CAGR of 20% between 2003 and 2020, along with a considerable increase in its commercial network (in 2013, it had 6 thousand distributors and 60 thousand associates; today, there are more than 60 thousand and 1 million 200 thousand, respectively).

Its IPO was unique since it was the first Mexican company listed directly on Nasdaq. In 2019, the company agreed with DD3 Acquisition Corp to be listed through a SPAC, a company founded by Martin Werner and Jorge Combe, two former Goldman Sachs bankers specialized in Latin America. They were looking for a high growth and asset-light Latin American company, and they found it in Betterware.

And the reason that led Betterware’s management team to go public in the United States, instead of its country of origin, was that they saw few successful listed organizations like theirs in the Mexican stock market; mid-cap and high growth (recently, there have been stock delisting by other companies, such as Grupo Lala, IEnova or Santander).

Business model

Betterware de Mexico is dedicated to the direct sale (Direct-to-Costumer) of home organization products currently divided into six categories: kitchen, home, bedroom, bathroom, cleaning, and technology.

Within these categories, it has a wide range of products, ranging from 20 MXN (one dollar) to 1,700 MXN (almost 85 dollars). All these are offered in 9 catalogs per year, including around 400 products with high innovation, launching more than 300 new products annually.

The commercial network is divided into two tiers: distributors and associates. Betterware occupies the top of the process, later, then come the distributors who are the ones who connect with the associates, who have the role of selling to the consumer and being customers themselves.

The incentives to sell for both distributors and associates are that they acquire the products at a discount and when they are making the final transaction, they obtain the benefit by selling it to the consumer at a higher price. Therefore, they do not receive direct remuneration from the company. In addition, they have a reward plan with Betterware Points (exchangeable for company products or different benefits, even paid vacations).

Associates:

- 24% discount on purchases

- 1 Betterware point for every 1 MXN

Distributor (in addition to the above):

- From 12 to 16% discount on associate purchases

- From 44 to 55% of points earned by associates

Therefore, the business process is as follows:

- Associates send purchase orders to distributors

- These turn to Betterware

- The company ships the products to distributors

- The distributors are the ones who deliver the products to the associates and collect the sales produced, thereby paying Betterware

- The associates deliver the products to the end customer

Business pillars

Product innovation: They have a team of anthropologists, statisticians, and other professionals from different fields who analyze the data they receive to understand customer behavior. In addition, they receive feedback from intermediaries with a new app. To do this, they closely monitor and update the strategy based on data on a weekly basis.

The design department subcontracts some professionals, has a specialized design laboratory and collaborates with more than 12 universities for new ideas. These three things make it possible to launch 300 new products per year (the process for a new product usually takes between 5 and 9 months).

The technology: The app that communicates Betterware with sellers (distributors and associates) has just been updated to upgrade operations and receive feedback from the users. In December 2020, to reach new customers, they launched their e-commerce website, and in the first months, they had experienced extraordinary growth. Likewise, they bring technology to their products, including a new category (boosted by the acquisition of Gurúcomm, which we will discuss later).

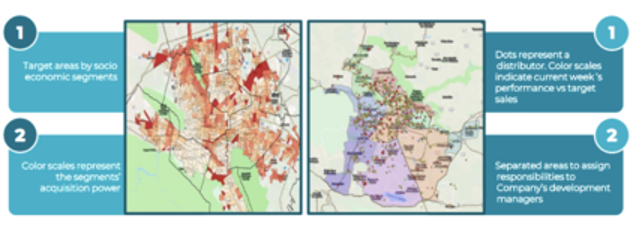

Business intelligence: Probably, one of the keys to Betterware’s growth. With all the data they receive through several channels, they locate exploitable geographical areas so there is no cannibalization and to strengthen those underrepresented areas. They use big data and weekly sales monitoring to adjust their objectives in real-time (they analyze number of orders per distributor, average ticket, best sellers, etc.), so they can improve their product offering.

It should be noted that, in 2021, they have completed the transfer of their employees (administrative, research, operations, etc.) to new headquarters in Guadalajara, with more than 70,000 sqm, capable of packing 1.5 M products per day, thanks to an automated process.

The company is not capital intensive because it outsources most of its supply chain. Manufacturing is made 90% in China and 10% in Mexico. All of them are certified by the company’s teams, to the point that, to maintain reasonable control over the production and quality of their products, they established an office in Ningbo, China.

International operations are carried out in US dollars (this is one of the risks that I will discuss later) and are transported mainly by sea to the port of Colima, where a single transport company (whose only client is Betterware) takes them to their distribution center in Guadalajara.

Products stay in the warehouse for an average of 80 days, where they are packaged to be sent to distributors throughout Mexico. They use 5 delivery companies (who also have Betterware as their exclusive client). Thanks to its two-tier distribution scheme, Betterware saves the last mile delivery cost (delivery to the end consumer is one of the biggest logistics problems, in some cases accounting for 50% of total cost) since associates are the ones who end up delivering the products to their customer. All this within 24-48 hours.

Mexico and Betterware, a perfect match

This business model fits perfectly with all the peculiarities of Mexican Market. Mexico’s geography combines densely populated urban centers with semi-desert areas in which the communities are small and spread out. Thanks to the last mile cost savings, the company can ship to any place without incurring high costs (unlike specific competitors such as Amazon or Mercado Libre).

On the other hand, it has focused on the ideal profile of sellers and customers. Most of its associates are women, who seek extra income either because cultural issues, they carry out informal work at home and seek some independence, or due to gender inequality and wage gap (during Covid-19, according to the INEGI, 84% of lost jobs were occupied by women). In addition, low salaries cause, in general terms, that workers occupy several jobs simultaneously.

Betterware’s target segments of the socio-economic levels are C and D, the middle and lower social class, accounting for 83% of the population. An essential point in the Mexican Government’s policies is aid to low-income families, which positively impacts Betterware’s performance.

Future Trends

The Company’s model relies on four trends projected into the future. Firstly, home organization; since houses are getting smaller, and the time that people spend in their houses increases (favored by home office). Also, a greater consciousness of cleanliness and organization is being generated.

Due to confinement, the Gig Economy (with more precarious, temporary, and telecommuting jobs), as well as technological solutions, are increasingly present in our lives, and Betterware is trying to align itself to take advantage of it. In addition, the closure of other business models gave them more visibility, demonstrated in their results.

Finally, Big Data, information processing, and the increasingly powerful tools for this are helping them improve market perception and more efficient response. They are using PowerBi for data processing and Knime for artificial intelligence, and they collaborate with Bain & Co. for data optimization of services, relocation, efficiency management, etc.

Growth

On one side, there is organic growth, the focus of the company. Currently, its penetration into Mexican households is 20%, and its Share of Wallet, also 20%, so the company is focused on strategies to increase them. They rely on the location of zones to increase their presence in certain areas and avoid conflicts between distributors.

Besides, with the release of its website, it aims to reach the upper segment of the population (which are those with better Internet access) and take advantage of the trend in e-commerce. All this without harming their sales network, since Betterware will carry out the operations in two ways: the sale is automatically assigned to the closest distributor, or the customer enters a personalized link of their seller, who will automatically be assigned the sale. With this new selling tool, the commercial network is not affected since it doesn’t matter whether the operation is done traditionally or electronically; they will receive the same benefits.

To be in a better position and have greater visibility, in January 2021, they launched their most ambitious marketing campaign until now.

Inorganic growth will be based on two pillars: acquisitions of companies to offer new product lines and international expansion, which will also be supported by agreements and investments with critical partners.

Acquisitions

On March 22, 2021, Betterware de México acquired GurúComm for MXN 75M (or USD 3.5M). However, it will take 3-4 years to have a material impact on Bettwerware’s results.

With this operation, they reinforce their technology capabilities. Its implementation will be carried out in three phases, at the end of 2021, 2022, and 2023, respectively.

First, they will focus on offering distributors and associates an Internet and mobile subscription plan in order to generate recurring revenue. At first glance, this step seems not very efficient, as The company steps outside its core competencies. And to this, we must add that it is a complex market in Mexico, in which Telcel accounts for 60% and is a preponderant provider, not wholly open to competition (as it could monopolize supply).

In addition, in my personal experience, apart from Telcel, only AT&T offers an excellent mobile coverage service, since Movistar, being one of the larger companies, has a quality that could improve significantly, as well as other Internet providers leave much to be desired. However, since 2017, the government launched the Altan Redes project to manage a shared network and avoid these differences in service quality. Betterware intends to take significant advantage with this move. We will have to keep an eye on its evolution.

The other phases are more in line with their business model, as they will first offer, through their new Betterware Connect brand, technology solutions for the home, such as modems, repeaters, and others. The last phase will focus on other types of home technology applications, but this is not yet well defined.

International expansion

In 2020, they expanded to Guatemala as a pilot test, and as of March 2021, they began operating as Betterware Guatemala (they have not yet applied their policy 100 %). In this short time, they already managed to be profitable and experienced growth in 1Q21 of 382 % in Revenues year over year.

The company believes that its business model is easily replicable in other Latin American countries and the Guatemala test shows that it can be done. Therefore, its short-medium term objectives are to expand into Peru and Colombia. These two markets have a population structure and culture like Mexico and are 2/3 the size of the Mexican market.

Therefore, a positive future is looming for the company.

Market, competitors, and expectations

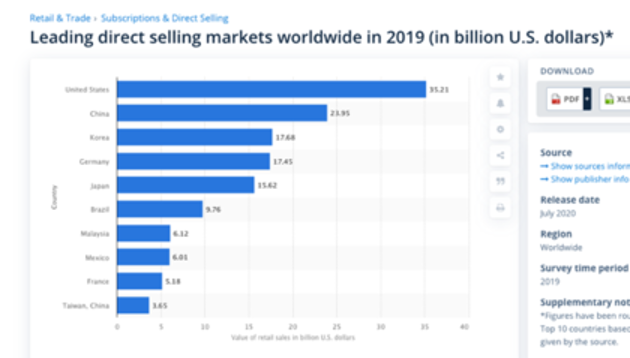

Mexico is among the ten most important markets for direct sales (Direct-to-Consumer), with a value that ranges between $6 and 7B dollars, and the second largest in Latin America. In addition, recently, it has had growth of more than 25% per year; however, this market is very heterogeneous.

The other companies of great importance that participate in this market in Mexico are Andrea (market leader, specializing in clothing and products for women), Avon (cosmetics and perfumes), and Mary Kay (like Andrea).

Other competitors such as Herbalife Nutrition, Cklass (Mexican footwear), Chemisette (thermal clothing and oils), and Tupperware, who may be the most similar to Betterware; however, it specializes in products only for the kitchen.

According to data from Euromonitor, this market will continue to grow at 9%, but segments such as shoes and accessories have a downward trend, while cosmetics are stagnant (partly affected by Covid and less use of makeup).

That said, there is no specialist rival in most of Betterware’s product lines (except Tupperware´s kitchen line) and having solutions for multiple areas of the home puts them first. Although other large companies such as Amazon or MercadoLibre could take away part of their market, their advantage due to their business model and the savings in logistics costs makes it likely to maintain high growth in the coming years.

IKEA

The Swedish company should be mentioned in this article for several reasons. Its business is one of the world’s best known success stories, and its origin has certain similarities with Betterware as its founder Ingvar Kamprad began the sale of furniture and household items by catalog and shipments by mail. However, the most relevant reason is its recent arrival in the Mexican market.

Rumors have existed since 2003, but it was until 2020 when it arrived in Mexico. First, it was launched exclusively as an online store, and in April 2021, it opened its first physical store, which slightly changes the traditional concept. Instead of being in a large area, they did it in a mall in Mexico City.

They intend to open five new stores throughout the country, positioning itself as a main competitor, and so it is another fact to be aware of, because although it specializes in furniture of larger volume than Betterware, there is an intermediate and low range line which coincide with Betterware, but the associate-client relationship can be a point in favor of the Mexicans not losing their advantage.

Risks

One of the most significant risks is the Mexican peso-US dollar exchange rate. All sales and figures in the company’s financial statements are in Mexican Pesos, but when listed directly on Nasdaq, its share price depends on the exchange rate. In addition, by importing almost all its products from China, most of its operation is done in USD, so the company’s gross margin is considerably affected by the variation of currencies. Even so, they try to reduce their impact with a hedging policy through Forwards.

Their imports are carried out mainly by sea transport, although they also use cargo planes. Therefore, shipping costs from China are a relatively essential item and more so in 2021, as there were collapses and delays in Chinese ports, which has increased those expenses. The company is aware of it and has contemplated it in its plans, they affirm that this increase will not continue forever, it will only prolong for a few months until normality returns.

Another critical aspect of the company’s performance is the political environment in Mexico. Usually, the country has been very liberal in its policies, facilitating entrepreneurship and economic growth; however, the current president follows a different line (although he has lost some power in recent elections).

In addition, its sales have always been highly correlated to the growth of this network, which could have lower growth, and maybe almost saturate the market. In addition, the economic impact caused by COVID must be considered. However, during the first quarter of 2021, things practically came back to normal and Betterware outstanding performance.

Lastly, the company’s ventures into new countries may not be as successful as expected and lower the growth expectations for Betterware, but the initial step they have taken in that direction has been successful.

Corporate Governance

The company has a very family-oriented character, with Luis Campos as the president after purchasing it in 2001, his sons, Andrés Campos, the CEO, and Santiago Campos on the Board of Directors.

Luis, prior to the purchase, already had extensive experience in the direct sales market in Mexico. His son Andrés, with an excellent background at one of the best universities in Mexico and the United States, has held several management positions at the company before being elected CEO in 2018. Additionally, there have been recent changes in the company’s key positions (CFO, CIO, and chief strategy officer) as well as the participation in the boards of the directors of DD3.

51.3 % of the company is held by Campalier SA, which exclusively holds the shares. 34.14 % was owned by Promotora Forteza, an investment vehicle that merged with Betterware, passing their shares into the hands of 18 individual investors, which, according to the company itself, are long-term committed investors. Finally, the percentage of free float is small because part of the remaining 15% belongs to DD3.

That is why the “skin in the game” of board members is very significant, and so far, the decisions they have taken have been highly successful, having among their priorities the remuneration of shareholders with considerable dividends. Always conscious with their decisions, never in a hurry to execute them, such as the international expansion or the implementation of GurúComm.

Recently, they created Fundación Betterware (in 2018) to connect with the most disadvantaged communities to carry out projects in partnership with them, to convey values of respect and honesty and produce a positive impact.

Also noteworthy is their new headquarters, a modern building for its automated distribution chain and administrative and creative staff workspaces, with open spaces that encourage sharing, enhance communication, and thus streamlining the processes.

In addition, to support their workers, they have numerous facilities, such as daycare, medical and beauty care, healthy dining rooms, gym, and green spaces, with the intention of modernizing their work environment, following successful steps taken by other large corporations such as Google.

Financial statements

Before evaluating their financial statements, there are several issues to highlight. In the first place, the transition from a private to a public company has dramatically modified its image in the first years, leaving 2018 distorted in matters such as Stockholders Equity. On the other hand, they recognize the low quality of certain internal controls, although Deloitte audits the accounts.

Balance Sheet

The company’s working capital is positive and growing, although its weight in the balance sheet does not vary that much. While the company’s structure had a significant change with a more significant net worth (going from 5% in 2018 to 20% in 2020).

The remarkable growth of total assets with its entry into the stock market has also normalized the size of intangible assets, as they currently stand at 15% (after being 45% in 2018).

It has a significant cash position (in part because it is a requirement of the loans it has acquired), and therefore, the company has Negative Net Debt.

In its current liabilities, the essential item is that of suppliers, since the company has a policy of payments to manufacturers in China of 120 days, which it has persevered despite the pandemic; while customers make their payments in a maximum of 30 days (distributors are usually given two weeks of credit).

Profit and loss account

In relation to this financial statement, there is another point to be made. Throughout 2020, due to the IPO and the Warrants agreement the company made, they had losses due to the change in the value of these nearly one billion pesos, which caused that, when wanting to carry out the exchange, they had to issue additional shares, with consequent dilution. Another situation to highlight is the unrealized losses on derivative instruments of almost 300 million. Both had no monetary impact, so they did not affect the company´s cash flow. Therefore, they will be excluded from having a more representative image of the business in the future.

Their sales have grown 60%, 33% and 135%, respectively, in the last 3 years. During the pandemic, not having to close their business, thanks to being considered an essential industry, due to their cleaning products and their business model made them benefit considerably from COVID. That has given them great visibility.

The gross margin for the last year decreased by 4% due to the peso’s depreciation throughout the crisis, which hurt them in purchasing products from China. In the first quarter of 2021, the normalization of exchange rates benefited them more than the impact of the increase in freight rates.

Their interest rate is actually high (approximately 13%), but we must remember that in Mexico, the cheapest loans in mortgages are above 8-9%; that is why that premium is understood. At the same time, the tax rate is around 30%, with the threat that the government will increase it in the future, although it does not seem likely.

| 2018 | 2019 | 2020 | |

| Gross Margin | 58,63% | 58,48% | 54,67% |

| Net Income Margin | 12,92% | 15,31% | 20,36% (4,66%) |

| ROE | 372,85% | 172,01% | 160,31% (36,70%) |

In parentheses are the figures without excluding the impact of warrants and derivatives. You can see what a fantastic company it is, with extensive margins for the business model and the products they sell.

| 2018 | 2019 | 2020 | |

| Payout | 78,57% | 72,64% | 56,16% (245,30%) |

| PER (Net Profit 2020 and Market Cap a 21/06/2021) | 20,91 (91,90) |

If one were to look only at their financial highlights, without delving deep a company with a Price-to-Earnings Ratio of more than 90 times and a dividend payout of more than 200% would seem like a dangerous company to invest in. However, after these two adjustments, the picture is more logical. In addition, the dividend has increased consistently in recent years, for a 2021 dividend yield of approximately 4%.

Cash Flow Statements

Due to the activity itself, the company has generated profits in the last three years, and it has increased six-fold since 2018. The company has continued to invest, mainly due to the construction of its new headquarters. In 2021, the company expects Capex spend of almost 500M, 80% related to that property, while the rest is distributed in additional equipment and technology. This capital investment represents around 5% of the company’s net revenue.

Despite the IPO carried out and the granting of new loans to supplement and regulate the interest rate they had, the flow of financing has remained negative. Overall, Betterware appears to be managed in a very responsible manner.

The guidance of the company for 2021 is:

| Guidance | 2021 |

| Net Revenue | 10,100 – 11,100 (∆39-53%) |

| EBITDA | 3,000 – 3,300 (∆39-53%) |

| EBITDA Margin | 29.7% (fall of 10 bps) |

In the 1Q21 Earnings Release, Betterware said that given the strong start to the year, they expected to close towards the upper end of their outlook.

Valuation

I discovered this company in the Peter Lynch style because in my close circle, there are Betterware distributors and, therefore, a lot of consumption of their products (due to that distributor-client relationship). Their products are excellent and versatile home solutions, and their quality is quite acceptable.

Once I found out that the company went public, I analyzed and invested in it, which I wanted to communicate before talking about the valuation.

Using a DCF model is very complicated and minimum variations could change the valuation considerably. So, for the projection we must take in mind the high optionality of Betterware (the success in Mexico, new acquisitions, and international growth).

Therefore, it has been decided to project a normalized profit for 5 years, with several basic assumptions. First, they will likely double their penetration into Mexican homes, which is the company’s goal, and with each quarter they report, it seems that they will achieve it sooner. In addition, they want to increase their share of wallet, and by including technology products and higher margins, they will be able to achieve this partially. So, the company’s organic growth is projected to increase 240 % in 5 years (in 1Q21 it increased its sales by 229 %).

If they can carry out their international expansion with moderate success, this could increase an additional 15-20%. The company’s original goals are: 75 % in Colombia and up to 88 % in Peru, so if it is developed with the same caution and efficiency, it could give the company an extraordinary journey in the future.

With these assumptions, the CAGR of sales could range between 22% and 30%, well below what it has had between 2017 and 2020 (71%), with a relatively positive impact of the pandemic.

Even so, a margin expansion has not been projected, placing them between 17% and 20%. Given the exchange rate problem, we do not like to predict the currency market. Therefore, we apply a premium of 10% compared to the current one, about 22 USDMXN.

Definitively, it is a company with excellent know-how and business intelligence in the Mexican market, which gives it a significant advantage over a new possible competitor. However, they have no other barrier to prevent another competitor from entering the market and taking share, no lasting competitive advantage, or patents. For this reason, a multiple of 12 is applied to normalized profit since it is still a business that fits perfectly with the Mexican economy.

The valuation, considering the different scenarios that have been raised, could be between 60 and 70 USD per share.

Betterware is a company that has been able to adapt its business model to the characteristics of the market in which it operates, with a management team with a long track record and great success, which takes care of their shareholders and have benefited from the latest events to establish themselves in the market. It has a long way to go and probably a bright future.

(This is not a recommendation to buy or sell, this is only my vision of the company and its market, so I always suggest doing your own analysis).

Contact:

Twitter: @IPOEdge