CrowdStrike (CRWD): Great Company, Brutal Price

By IPO Edge Editorial Staff

An outage took down half the internet in July 2024. The company behind it was CrowdStrike (CRWD).

Two years later, the stock has not just recovered. It has climbed to fresh records.

Last week’s first quarter results explain why, with record net new annual recurring revenue and the company’s first GAAP profit in years.

CrowdStrike also announced a four-for-one stock split, a move that tends to draw retail crowds.

Never Miss our Weekly Highlights HERE

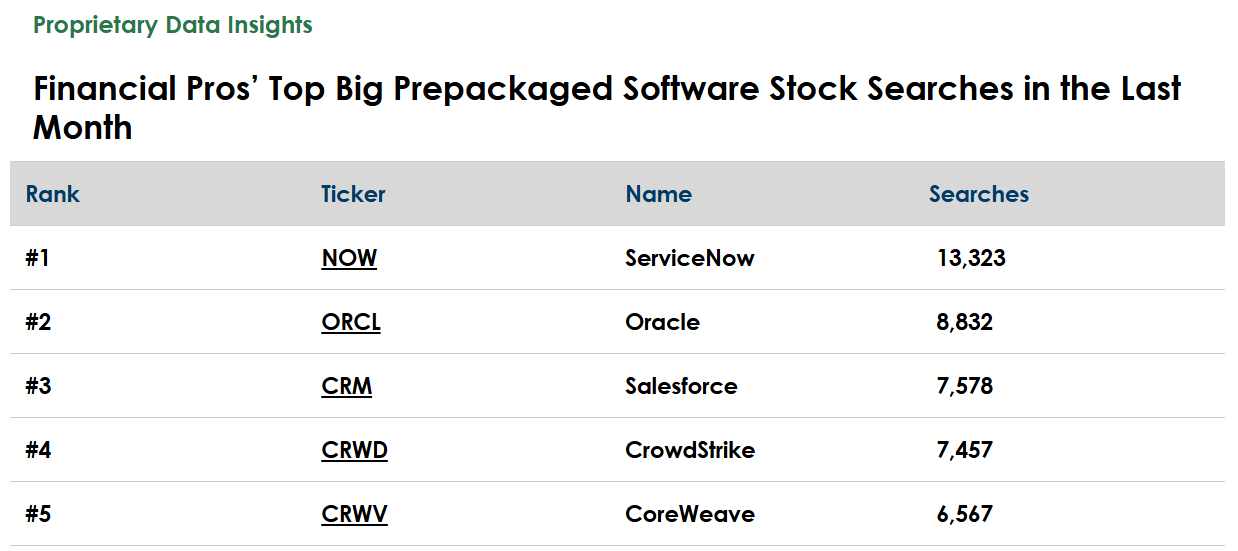

Financial pros noticed too, ranking CRWD fourth among big software names in our TrackStar data, just behind ServiceNow (NOW), Oracle (ORCL), and Salesforce (CRM).

The pitch is simple. CrowdStrike wants to be the security layer for the entire AI buildout.

The question is whether that justifies one of the richest valuations in tech.

CrowdStrike’s Business

CrowdStrike sells cloud-delivered cybersecurity through its Falcon platform. A single lightweight agent guards laptops, servers, identities, and cloud workloads.

The model is subscription-first, and customers add modules over time. More than half now run six or more modules.

It serves enterprises, governments, and small businesses worldwide, and counts a large share of major corporations as clients.

CrowdStrike segments its business into the following areas:

- Subscription (95% of total revenues) – Recurring access to Falcon platform modules across endpoint, cloud, identity, and data security

- Professional Services (5% of total revenues) – Incident response, advisory work, and threat hunting engagements

First quarter revenue rose 26% to $1.39 billion, with net new ARR up 32% to a record $256 million.

GAAP net income swung to a $27.8 million profit, reversing a $104.3 million loss a year earlier.

READ MORE

Highlights: Tech Edge at Pax8 Beyond 2026 in Salt Lake City

Management is leaning hard into artificial intelligence. It launched Project QuiltWorks, a coalition with OpenAI and Anthropic aimed at frontier AI risk.

It also rolled out Charlotte AI AgentWorks, a no-code tool built with AWS, NVIDIA, and OpenAI for custom security agents.

The Falcon Flex consumption model keeps expanding too, now reaching the full services portfolio.

These moves push CrowdStrike beyond endpoint protection toward a platform that customers consolidate spending onto.

Financials

Source: Stock Analysis

Revenue climbed from $481.4 million in fiscal 2020 to $5.1 billion over the trailing twelve months.

Growth has cooled from triple digits to 23.2%, which is still impressive at this scale.

Gross margins sit near 75%, but heavy spending on sales and research keeps the operating margin slightly negative at -4.3%.

READ MORE

Suja Life Sees 66% EBITDA Growth as Functional Beverage Boom Accelerates

The cash story is the real headline. Free cash flow reached $1.5 billion, a 29.6% margin, while operations threw off $1.8 billion.

The balance sheet is pristine, with $4.6 billion in cash against just $745.8 million in long-term debt.

CrowdStrike pays no dividend, choosing to reinvest everything into growth.

Valuation

Source: Seeking Alpha

Here is where the story gets uncomfortable.

CrowdStrike trades at 156.9x trailing non-GAAP earnings, while ServiceNow sits at 29.1x and Salesforce at just 12.7x.

On sales, CRWD fetches 31.9x versus 9.1x for Oracle and 3.8x for Salesforce.

Price to cash flow tells the same tale at 90.3x, far above every peer on this list.

READ MORE

The Spill: Is Broadcom (AVGO) the Other AI Trade?

Continued…

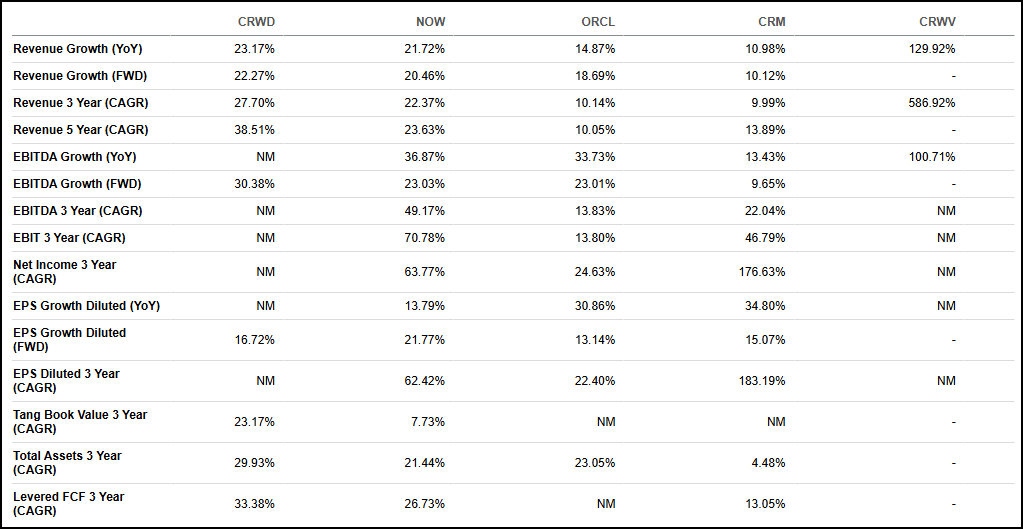

Growth

Source: Seeking Alpha

Growth is what investors are paying for, and CrowdStrike delivers.

Its 23.2% revenue growth tops ServiceNow, Oracle, and Salesforce, trailing only hyperscaler CoreWeave (CRWV).

Over three years, revenue compounded at 27.7%, the best of the established group.

READ MORE

Fluence Scores Independent Validation of Industry-Leading Battery Storage Reliability

Levered free cash flow growth of 33.4% over that span also leads ServiceNow and Salesforce.

Forward EPS growth of 16.7% lags ServiceNow, a reminder that profit expansion may slow.

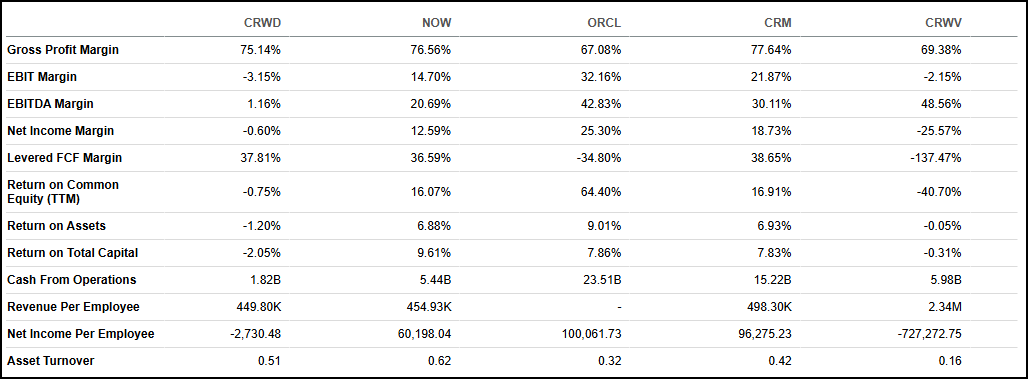

Profitability

Source: Seeking Alpha

CrowdStrike’s 75.1% gross margin lands in the middle of the pack.

Its operating margin remains negative at -3.2%, well behind profitable peers like Oracle and Salesforce.

Yet the levered free cash flow margin of 37.8% nearly matches Salesforce and beats ServiceNow.

In other words, the GAAP losses mask a business that gushes cash.

READ MORE

The Spill – Campbell’s (CPB): The Only Grower Nobody Wants

Our Opinion 6/10

CrowdStrike is a wonderful company attached to a frightening price.

The growth is real, the cash flow is excellent, and the AI security tailwind looks durable.

But at 156.9x earnings and 31.9x sales, the stock prices in years of flawless execution.

Any stumble, and the downside could be severe.

We love the business and would happily own it after a meaningful pullback.

For now, the valuation keeps us on the sidelines.

Contact:

Click HERE to follow us on LinkedIn