Ralph Lauren (RL) Just Crushed It. Now What?

By IPO Edge Editorial Staff

For nearly 60 years, the polo pony has stood for old-money Americana. Now it’s quietly become one of the best-performing names in apparel.

Ralph Lauren (RL) just blew past $8 billion in annual revenue for the first time in company history.

Q4 sales jumped 17%. Full-year adjusted EPS climbed to $16.59 from $12.33. The board hiked the dividend 10%.

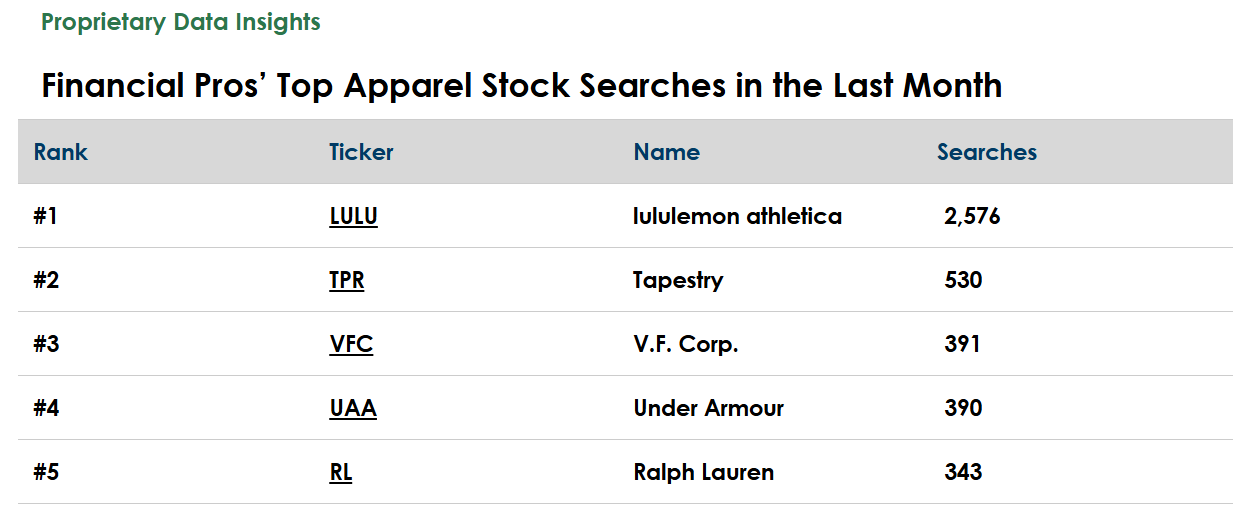

Yet RL ranks dead last on our list of most-searched apparel names, well behind lululemon (LULU), Tapestry (TPR), V.F. Corp. (VFC), and Under Armour (UAA).

That’s despite RL trouncing every one of them on growth and margin expansion.

Investors may be sleeping on this one. Or the premium valuation may be the catch.

Ralph Lauren’s Business

Ralph Lauren designs, markets, and distributes luxury lifestyle products spanning apparel, accessories, home, and fragrance. The brand sells aspirational Americana to a global audience, with the polo pony recognized in over 100 countries.

The company operates more than 540 directly run stores and 730 concession shops worldwide, sells through department stores like Macy’s and Nordstrom, and runs a fast-growing direct digital business. It added 6.5 million new DTC customers in FY26 alone.

Ralph Lauren segments its business into the following areas:

- North America (41% of total revenues) – Brick-and-mortar stores, digital commerce, and wholesale relationships across the U.S. and Canada

- Europe (31% of total revenues) – Retail stores, e-commerce, and wholesale partnerships across Western and Eastern Europe

- Asia (26% of total revenues) – Stores, concessions, and digital sales across China, Japan, Korea, and Southeast Asia

- Licensing & Other (2% of total revenues) – Royalties from licensed product categories and partnerships

The May 21 earnings report capped a banner year. Q4 comp sales rose 17% with mid-teens AUR growth, signaling consumers are paying full price rather than waiting for markdowns.

Asia led the charge with 31% reported growth, fueled by exceptional Lunar New Year sales in China. Europe grew 18% on a reported basis. North America rose 8% with double-digit DTC comps.

The strategy under CEO Patrice Louvet is called “Next Great Chapter: Drive.” It centers on brand elevation, AUR expansion through full-price selling, key-city ecosystem buildout, and category extensions in women’s, outerwear, and handbags.

The newest handbag line, Polo Blaze, debuts in Fall ’26 at Paris Fashion Week.

Investment is ramping. Capex nearly doubled to $408 million in FY26 as RL bought select real estate and opened stores in Chengdu, Sydney, Bangkok, Newport Beach, and London.

Financials

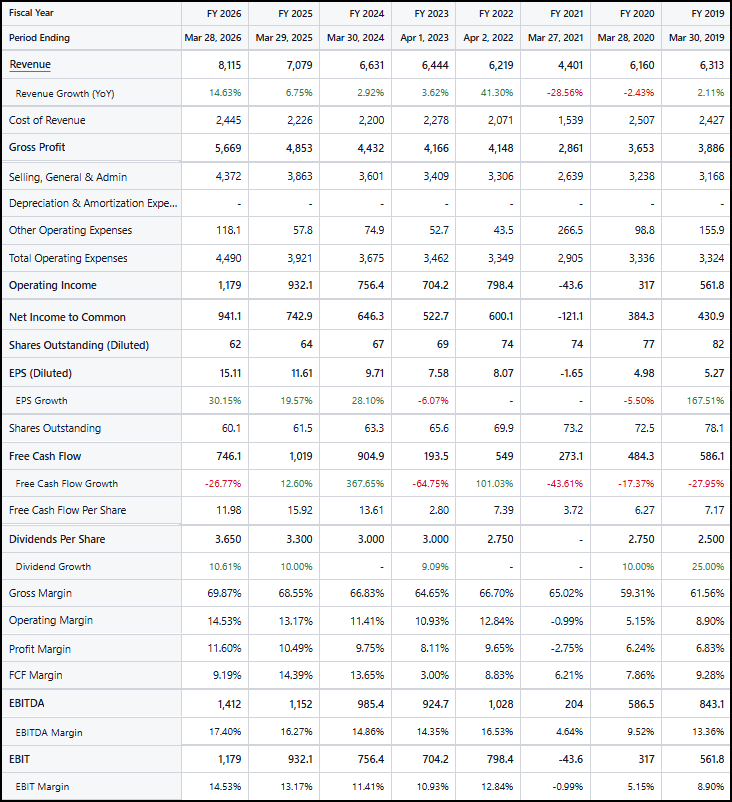

Source: Stock Analysis

Ralph Lauren grew FY26 revenue 14.6% to $8.1 billion, a meaningful step up from 6.8% growth in FY25 and 2.9% in FY24.

Gross margin expanded to 69.9% from 68.6% the year before, driven by favorable mix, AUR growth, and lower cotton costs offsetting U.S. tariff headwinds.

Operating margin jumped to 14.5% from 13.2%, and net income rose to $941.1 million from $742.9 million.

Free cash flow came in at $746.1 million, down 26.8% from FY25’s $1.0 billion. The drop reflects the doubling of capex rather than any deterioration in the underlying business.

Operating cash flow of $1.15 billion still comfortably covered the $408 million in capex, the dividend, and a chunk of the $500 million in buybacks.

The balance sheet is in great shape with $2.1 billion in cash and short-term investments against just $1.2 billion in total debt. Inventory is up only 7%, well below sales growth.

Valuation

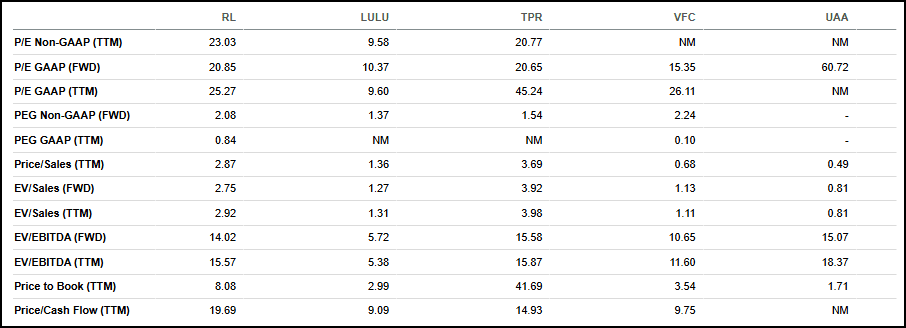

Source: Seeking Alpha

Ralph Lauren trades at 23.0x trailing earnings and 20.9x forward earnings, a sharp premium to lululemon at 9.6x and 10.4x.

Tapestry sits right alongside RL at 20.8x trailing and 20.7x forward.

On EV/EBITDA, RL fetches 15.6x trailing versus LULU at just 5.4x and TPR at 15.9x.

Price-to-cash-flow tells the same story. RL trades at 19.7x, more than double LULU’s 9.1x.

The premium reflects RL’s accelerating growth, but it leaves little room for disappointment.

Continued…

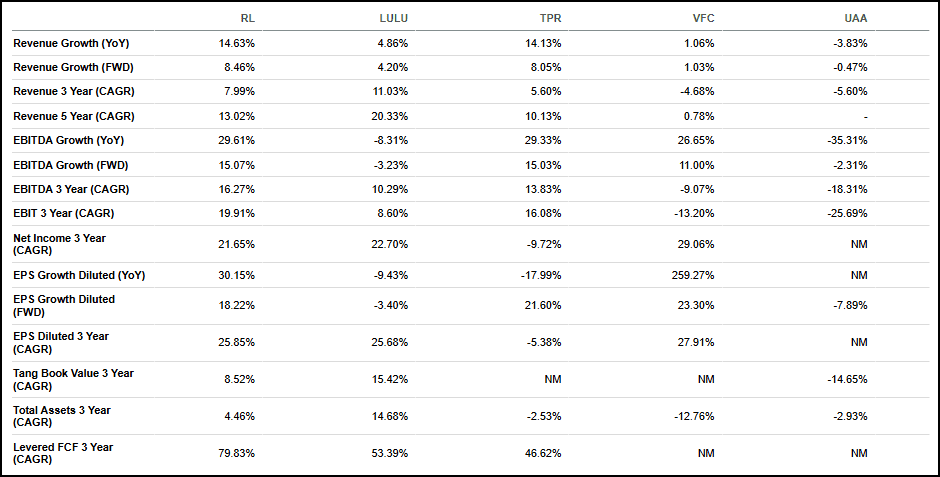

Growth

Source: Seeking Alpha

Ralph Lauren’s 14.6% revenue growth lapped LULU’s 4.9% and edged out TPR’s 14.1%. VFC managed just 1.1% and UAA shrank 3.8%.

Forward revenue growth of 8.5% also tops the group.

EBITDA growth of 29.6% year-over-year crushes LULU’s negative 8.3%. EPS grew 30.2% diluted, far ahead of LULU’s 9.4% decline and TPR’s 18.0% drop.

Over three years, RL’s levered free cash flow CAGR of 79.8% leads every peer.

Profitability

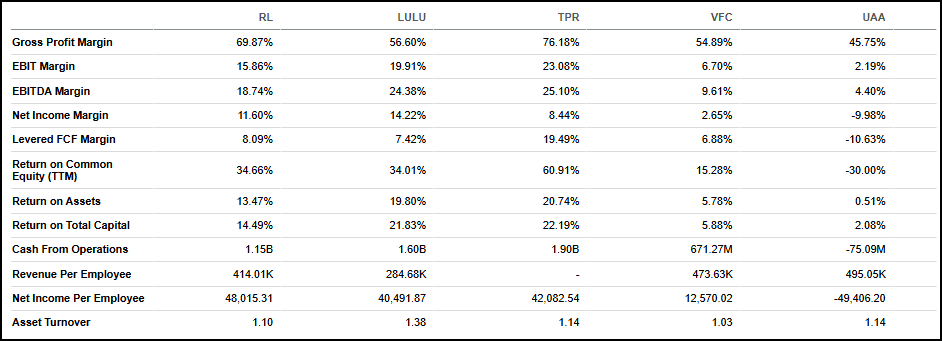

Source: Seeking Alpha

Ralph Lauren posts a 69.9% gross margin, well above LULU at 56.6%, VFC at 54.9%, and UAA at 45.8%. Only Tapestry tops it at 76.2%.

Where RL trails is operating leverage. EBIT margin of 15.9% sits below LULU’s 19.9% and TPR’s 23.1%.

Levered FCF margin of 8.1% beats LULU’s 7.4% but lags TPR’s 19.5% by a wide margin.

Return on equity of 34.7% is strong, edging LULU’s 34.0% but well behind TPR’s 60.9%.

Our Opinion 7/10

Ralph Lauren is executing better than at any point in recent memory.

The brand is resonating globally, pricing power is real, and the balance sheet is fortress-strong with a rising dividend and active buyback.

But the valuation premium over lululemon at half the multiple is hard to ignore. LULU’s struggles serve as a warning about what happens when apparel premiums unwind.

We’d hold RL for those already in. New buyers should wait for a pullback before paying 23x for a fashion brand at its cycle peak.

READ MORE

Save the Date: 2nd LA CorpGov Forum Sep 18 Featuring Sports, Entertainment & M&A

Never Miss our Weekly Highlights HERE

Contact:

Editor@IPO-Edge.com

Click HERE to follow us on LinkedIn