Meta (META) Is Spending Like Its Life Depends on It

By IPO Edge Editorial Staff

Last month, Meta Platforms (META) posted its fastest revenue growth quarter since 2021.

The stock fell anyway.

Revenue jumped 33% to $56.3 billion. Operating margin held at 41%. Net income climbed 61%.

Then management told investors that 2026 capex would land between $125 and $145 billion, up from a prior range of $115 to $135 billion.

Shares dropped roughly 7% after hours.

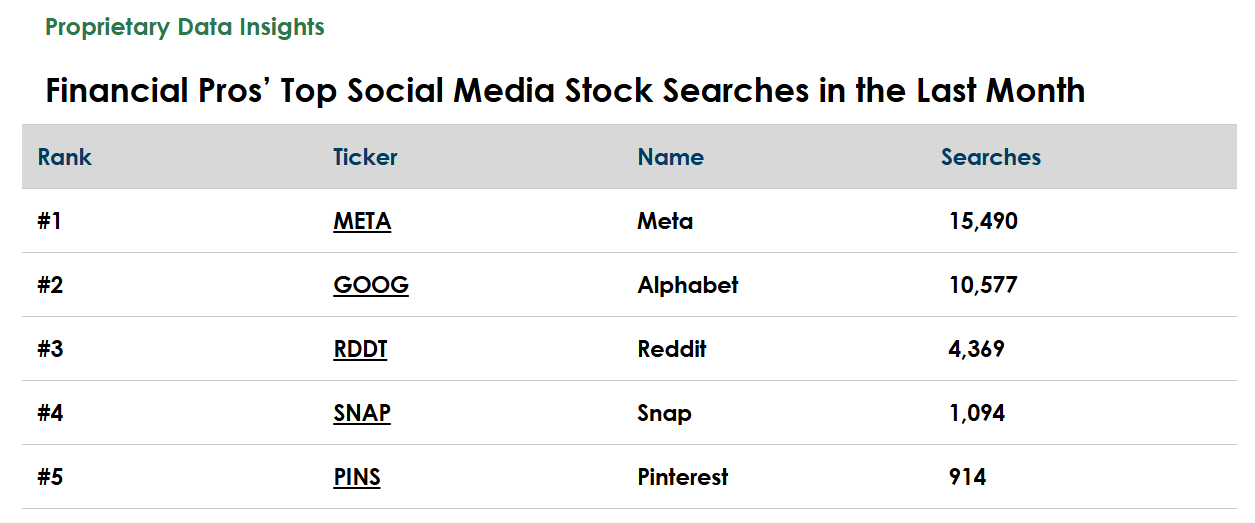

Search volume from financial pros surged after the print, according to our TrackStar data, with Meta capturing nearly 50% more searches than Alphabet (GOOG).

The question isn’t whether the ad business is healthy. It clearly is.

The question is whether Mark Zuckerberg’s AI spending spree pays off before investors lose patience.

Meta’s Business

Meta owns four of the most-used apps on the planet: Facebook, Instagram, WhatsApp, and Messenger. Roughly 3.56 billion people open at least one of them every day.

The company turns that attention into ad dollars. Ad revenue hit $55.0 billion in Q1, with impressions up 19% and price per ad up 12% year over year.

Meta segments its business into the following areas:

- Family of Apps (99.3% of revenue) – Advertising across Facebook, Instagram, Messenger, WhatsApp, and Threads, plus WhatsApp paid messaging and subscriptions

- Reality Labs (0.7% of revenue) – VR/AR hardware including Quest headsets, Ray-Ban Meta and Oakley AI glasses, software, and content

The headline this quarter was Muse Spark, the first model from Meta Superintelligence Labs.

Zuckerberg called it the start of his push to deliver “personal superintelligence to billions of people.”

Meta also raised its 2026 capex range to $125 to $145 billion. That’s nearly double the $72.2 billion it spent in 2025.

Management cited higher memory pricing and additional data center capacity for future years.

To offset some of the cost, Meta announced it will cut roughly 8,000 employees in May and pull back another 6,000 open roles.

The company is also rolling out more than 1GW of custom silicon developed with Broadcom, alongside AMD chips, to reduce dependence on Nvidia.

Financials

Source: Stock Analysis

Meta’s top line is on fire. Revenue grew 26.2% over the trailing twelve months and 22.0% in 2025.

Gross margin sits at 81.9%, with operating margin at 41.2%. Both are near five-year highs.

Cash from operations hit $32.2 billion in Q1 alone, up from $24.0 billion a year ago.

But capex jumped to $19.8 billion in the quarter.

Free cash flow came in at $12.4 billion, only modestly above the $10.3 billion from the year-ago period.

The full-year picture is harsher. FCF growth turned negative 14.7% in 2025, and the trailing FCF margin has compressed to 22.5% from a peak of 32.9%.

Meta carries $58.7 billion in long-term debt against $81.2 billion in cash and marketable securities. The balance sheet is in fine shape.

The capital return story has shifted, though. Meta paid no share buybacks in Q1, down from $12.8 billion a year ago, while continuing its $1.35 billion dividend.

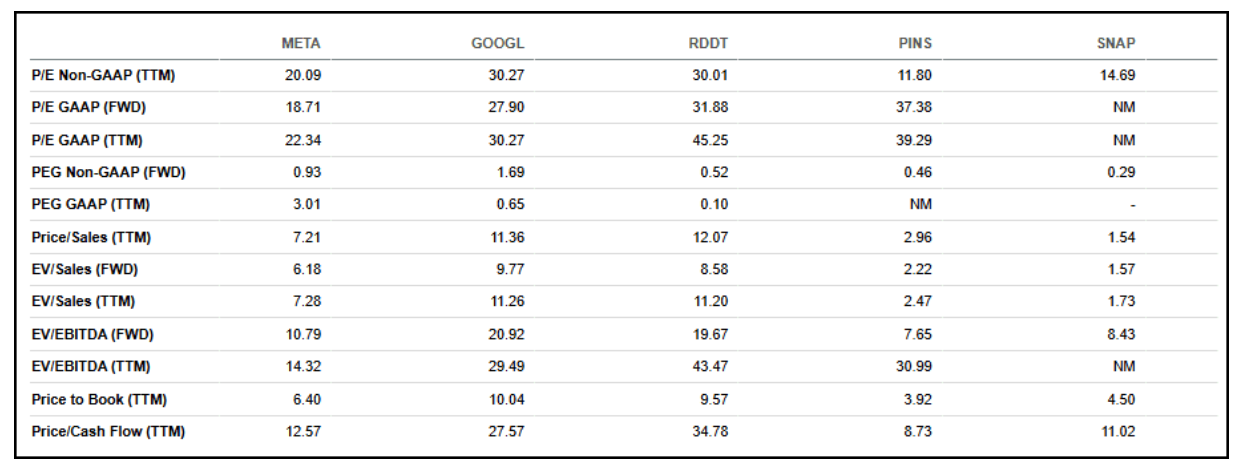

Valuation

Source: Seeking Alpha

Meta trades at 20.1x TTM non-GAAP earnings and 18.7x forward GAAP earnings.

That’s a meaningful discount to Alphabet at 30.3x TTM and Reddit (RDDT) at 30.0x.

On price-to-cash-flow, Meta sits at 12.6x versus 27.6x for Alphabet and 34.8x for Reddit.

The PEG ratio of 0.9 on a non-GAAP forward basis suggests the market isn’t giving Meta full credit for its growth.

EV/EBITDA tells the same story at 10.8x forward, well below Alphabet’s 20.9x.

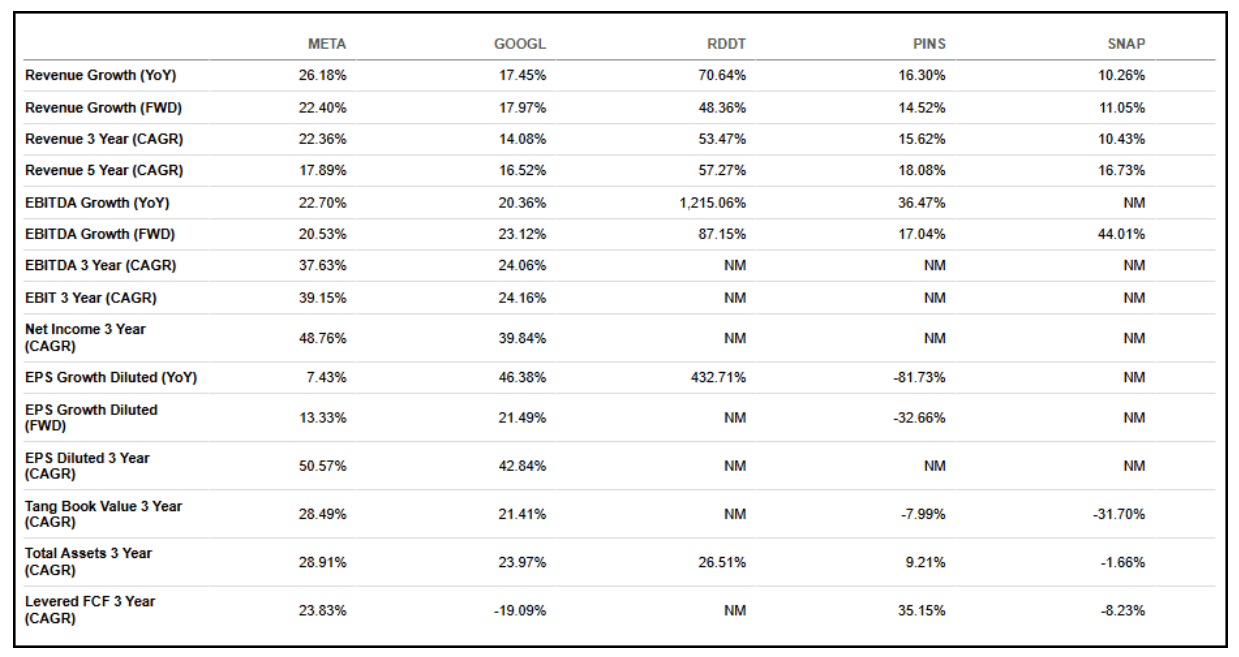

Growth

Source: Seeking Alpha

Meta’s 26.2% YoY revenue growth tops Alphabet’s 17.5% and trails only Reddit’s outlier 70.6%.

Forward revenue growth of 22.4% leads every name on the list except Reddit.

The three-year revenue CAGR of 22.4% beats Alphabet (14.1%), Pinterest (PINS) at 15.6%, and Snap (SNAP) at 10.4%.

EBITDA has compounded at 37.6% over three years, well ahead of Alphabet’s 24.1%.

Net income has grown at a 48.8% three-year CAGR, the cleanest profitability ramp in the group.

The one weak spot is diluted EPS growth, which slowed to 7.4% year over year as costs ramped.

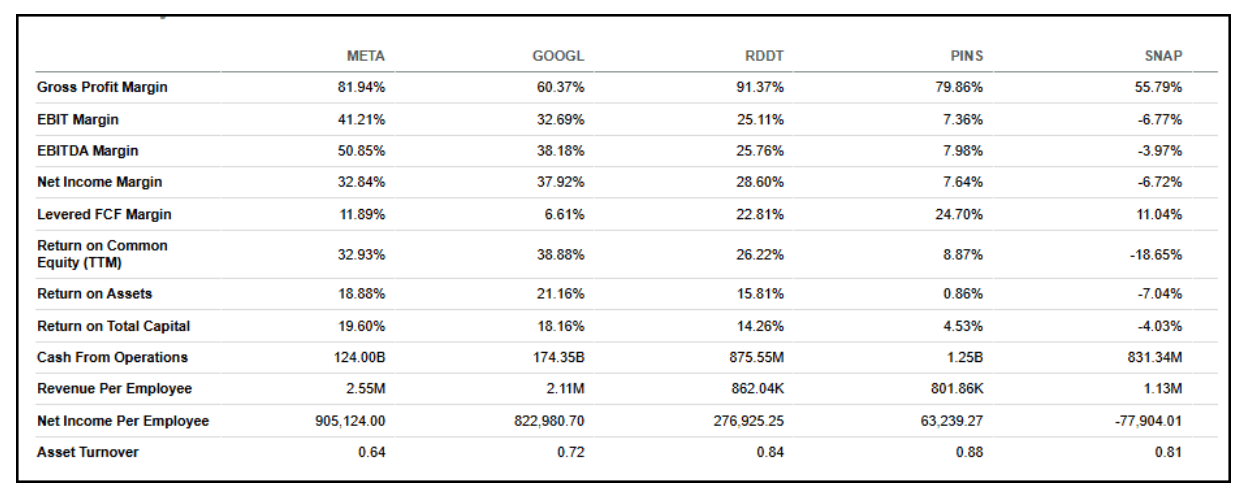

Profitability

Source: Seeking Alpha

Meta runs an 81.9% gross margin, second only to Reddit’s 91.4%.

Where Meta separates from the pack is operating profitability. EBIT margin of 41.2% dwarfs Alphabet (32.7%), Reddit (25.1%), Pinterest (7.4%), and Snap (-6.8%).

Net income margin of 32.8% is competitive with Alphabet’s 37.9% and well above the rest.

Levered free cash flow margin of 11.9% lags Pinterest (24.7%) and Reddit (22.8%), reflecting Meta’s heavy capex load.

Return on common equity of 32.9% is excellent, though slightly behind Alphabet’s 38.9%.

Our Opinion 7/10

Meta’s core advertising engine is performing about as well as any business this size can perform.

Margins are best-in-class. Engagement is climbing. Ad pricing is rising alongside volume.

The valuation discount to peers reflects one real concern: the $125 to $145 billion capex commitment.

If those AI investments compound into Reels monetization, ad targeting gains, and lower inference costs from custom silicon, the stock looks cheap.

If the payback stretches beyond 2027, free cash flow stays under pressure and the multiple stays capped.

We’d own it, but we wouldn’t add aggressively until there’s more clarity on AI ROI.

READ MORE

Final Panel Agenda and Closing Registration: 2nd Princeton CorpGov Forum May 21 – Endowments, Activism and Entertainment

Never Miss our Weekly Highlights HERE

Contact:

Editor@IPO-Edge.com

Click HERE to follow us on LinkedIn